.png)

.svg)

There’s this weird psychological trick some of us play on ourselves where we decide that the best time to start a new diet, routine, or budget is on a Monday. Or on the first of the month. Or on the first of the year.

Pretty crazy how that doesn’t apply to starting a new book, video game, or Netflix series, huh?

Yeah, that tactic is actually just a cleverly garnished cocktail of procrastination, anxiety, and dread.

The best time to start a budget is now—yes, even if it’s a Wednesday, or the 15th of the month, or the 11th month of the year. And here you are. Rock on! Studies show that you’re actually MORE likely to succeed with a new habit if you pick an arbitrary start day. Like today!

Think of it this way: if you start now, you’ll already be familiar with your new habit by the first of the month. Ahead of the game, even. If it was a race, you’d be leaving those, “I’ll do it later,” people in the dust…and who doesn’t love to win?

Get Ready: What You’ll Need to Begin

In reality, starting a budget in YNAB in the middle of the month is not more difficult. Money touches our lives every day—it’s not like all of our bills are due on the first, or like there’s some two day pause between months where everything resets perfectly.

Go gather up the following and meet us back here at the starting line:

- Your bank and credit card account log-in information

- Recent bank statements so you can estimate amounts and due dates of monthly bills

- A list of non-monthly bills with due dates, like your car registration, insurance payments, annual subscriptions, taxes, etc.

- An estimate of miscellaneous expenses that happen semi-regularly, like birthdays and holidays.

Ready to go the distance?

Get Set: Categories and Targets

The next step is to create categories and targets for each of your expenses. Think of your categories as envelopes full of cash. You’ll take a blank envelope, write “mortgage” on it, put the amount due and the due date in the corner, and fill that envelope with the appropriate amount of money before that due date rolls around.

But our way is much easier than shuffling paper money and digging around in envelopes to see how much you have.

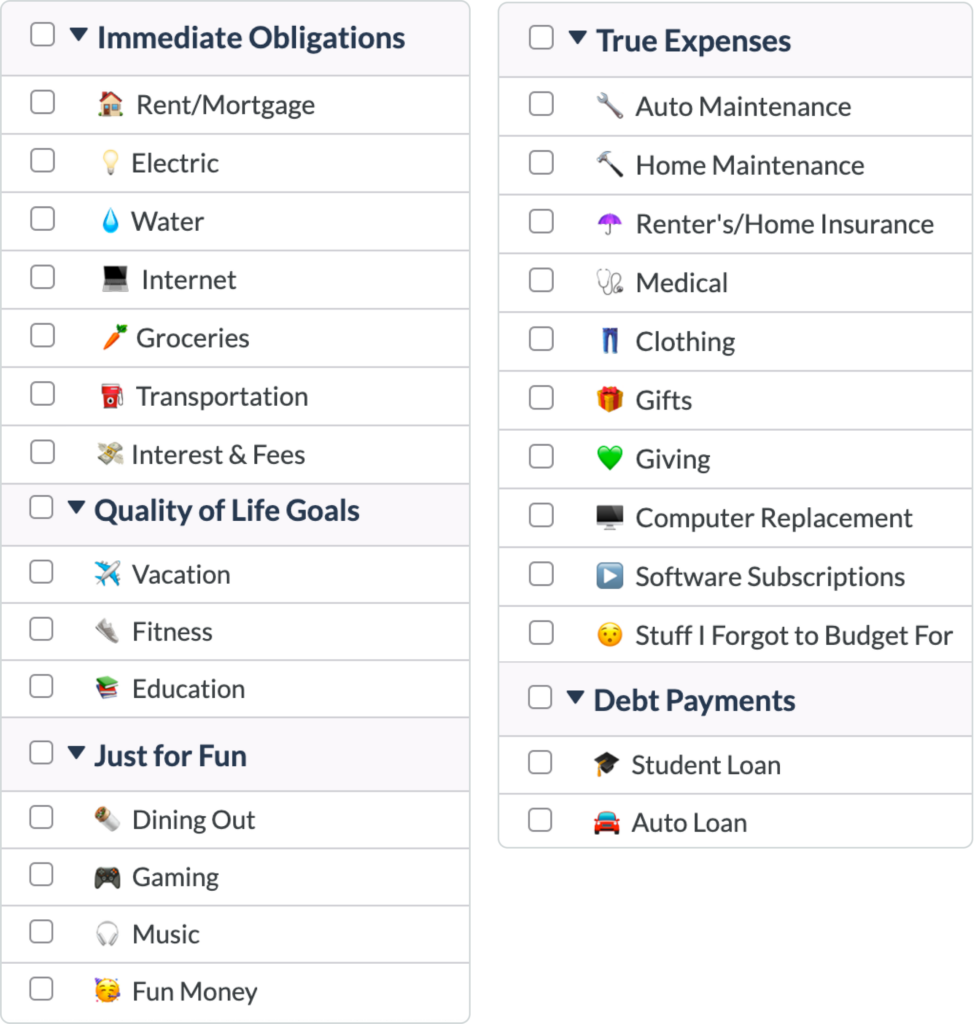

Categories

List your expenses as categories, and feel free to come up with a snazzy name or to add a cute emoji. You might as well make it fun. You can also organize your categories by due date so that you can visualize and prioritize your month more easily. Just drag and drop on the web app, or hit the “edit” pencil and long press on the three lines to drag and drop on mobile.

You can hide or delete categories if you get a little category-crazy. Just click on the category name on the web or on the minus sign in the edit screen on mobile to find those options. Your best bet is to keep your categories as simple as possible while you get started.

Targets

Step one of winning a race is knowing where the finish line is!

Probably. I don’t know because I don’t run but I really think this would be a critical component.

Anyway, spending and savings targets are like the finish line for funding your categories each month.

You can choose to set Weekly, Monthly, or By Date spending targets, depending on the type of expense:

- An expense like groceries might be a weekly target. You’d input your weekly spending limit and set a day of the week as your due date. YNAB automatically multiplies the assigned amount by the number of weeks in each month to turn it into a monthly figure.

- Your mortgage or rent payment would be a monthly expense.

- Holiday gifts, a vacation, or non-monthly expenses are good examples for when you might choose to set a “By Date” target with a deadline.

You set targets by hitting the edit pencil on mobile, or by clicking within the category on the web.

Go! Add Accounts and Assign Your Money

Now you’re really off to the races.

First, add your banking and credit card accounts to your budget.

Linked Accounts

You can choose to link your account to your budget and your balance and transactions will automatically update. (Yes, you can trust YNAB.)

Unlinked Accounts

If you’d like to be a little more hands-on with your money management, you can enter your transactions and input your balances manually. And actually, our teachers heartily recommend new YNABers enter their transactions yourself for the first week as you’re getting started.

Credit Cards

Don’t sleep on adding your credit cards to your budget, just make sure that you select Credit Card as the account type, because it changes the way you manage any existing debt.

Want to learn more about using credit cards in YNAB? It’s a popular request. Head on over to our blog post about YNAB and credit cards once you’re done setting up here.

Savings Accounts

It may be tempting to skip adding your savings accounts to your budget. It makes a lot of people nervous to see the money they’re trying not to spend show up in the “Ready to Assign” balance. The good news is that you’re still not going to spend it. You’re going to assign it to the specific category that you’re saving for—this protects that money, keeps it separate when you view your budget, and creates some accountability around meeting your savings goals.

Are you really going to borrow from your house downpayment fund for tacos for the second night this week? You’ll think twice about it when you have to move that money from one category to another.

Set up your savings account the same way you did for checking, just categorize it as a savings account when YNAB asks. (If you didn’t create savings categories upon your initial category set up, go do that now.)

Assigning Money Mid-Month

This is where the magic happens. Lace up your running shoes, my friends. (You don’t really have to wear shoes for any of this.)

The key ingredient to the YNAB method is…well, all of them. There are Four Rules, and they’re all important. However, Give Every Dollar a Job is the muscle behind your momentum.

Everything we’ve done so far has been warm up for this. Remember when you made your categories? Set your targets? Added your accounts? Now we’re ready to put each dollar to work.

See your Ready to Assign total at the top? That’s how much money you have to populate your budget with right now. Don’t worry about money you haven’t earned yet—those dollars will get their jobs when they actually show up to work.

Go down your list of categories in order of due date and/or urgency and ask yourself, “What does my money need to do before I get paid again?” Distribute your dollars between categories accordingly. Continue doing this until you reach zero in your Ready to Assign box. This is called zero-based budgeting and it helps you create more intention around spending your money.

Since it’s the middle of the month, you may need to check your bank statement to see which bills have already been paid so that you have a more accurate idea of which categories to fund first.

Also, if you’re halfway through the month, you can (probably) cut your grocery and dining out categories in half.

Step-by-Step Summary to Budget Success

So, basically we have Four Rules and three steps. To stay on the path to financial freedom, remember the following:

YNAB’s Four Rules

- Give Every Dollar a Job: Be the boss of your money. Tell each dollar what to do by assigning it to a specific category.

- Embrace Your True Expenses: Be realistic about your expenses. Accept that certain costs are going to pop up on an irregular basis and budget for those monthly.

- Roll With the Punches: Your budget is not set in stone. If you overspend in one category, move money from another category to cover it. Every time. Right away.

- Age Your Money: As you start being more intentional about your spending and saving, this month’s money will start to pay next month’s bills. No more paycheck to paycheck cycle!

The Three Steps Each Payday

- Step one: Add your income. When you get new money, put it in YNAB.

- Step two: Assign your dollars to categories. Ask, “What does this money need to do before more money arrives?”

- Step three: Track your spending, make changes where you need to, and check your budget before making spending decisions.

Budgeting works whether you start it on a Monday, a Wednesday, the first of the month, the fifteenth of the month, or midway through the 182nd day of the year.

The real key to budgeting is simply starting…so get ready, set, and go Give Every Dollar a Job.

Interested in more budgeting tips and tricks? Say no more. We’ll bring them straight to you in our Roundup.