.png)

At YNAB, we have rules. Yes. We. Do. (And they’ll do wonders for your bank balance—try them!)

… but beyond the rules, there are endless ways to customize your budget that we encourage you to explore. Case in point, cash management. Today, let’s look at two completely viable options. Which is better? Well, that’s up to you!

Option 1: The ‘Cash’ Category

If you don’t use a lot of cash, and you’re not worried about tracking precisely where every penny goes, then a ‘Cash’ category might be exactly what you need. With this no-fuss approach, you’ll record your cash withdrawal in YNAB, and then you’re done! Spend the cash however you like. Here’s how it works:

Step 1

Create a category for cash in your budget. YNAB has a default category called ‘Fun Money’. You can use that, or create a new category and label it ‘Cash’ (or whatever else tickles your fancy!).

If you share your budget with a partner, consider adding a separate cash category for each of you—like in the example, below, where we’ve labeled the categories “His Spending Money” and “Her Spending Money”.

Step 2

When you’re paid, budget money for your cash category. Our example couple has allocated 60 dollars, each, to cash:

Step 3

When you take cash out of the bank, record it in YNAB as an outflow and categorize it to your cash category. In our example, the woman has withdrawn 40 dollars:

Notice that now the budget shows that “Her Spending Money” only has 20 dollars left.

What About Cash Back?

This one can sometimes stump people, but it’s actually pretty straightforward. So, for example, if you ask for 20 dollars cash back on a 50 dollar purchase at the grocery store, simply record it as split transaction. It looks like this:

Once the cash is in your wallet, you’re free to spend it—there’s no need for further tracking or budgeting.

A Word of Caution

If you like a granular record of exactly where all of your money goes, this won’t work for you. Me personally? I’m okay with that because I don’t use a lot of cash. Plus, I set limits for how much I budget for this category. If I was spending $500 a month in cash and didn’t know where it was going? That’s a different story.

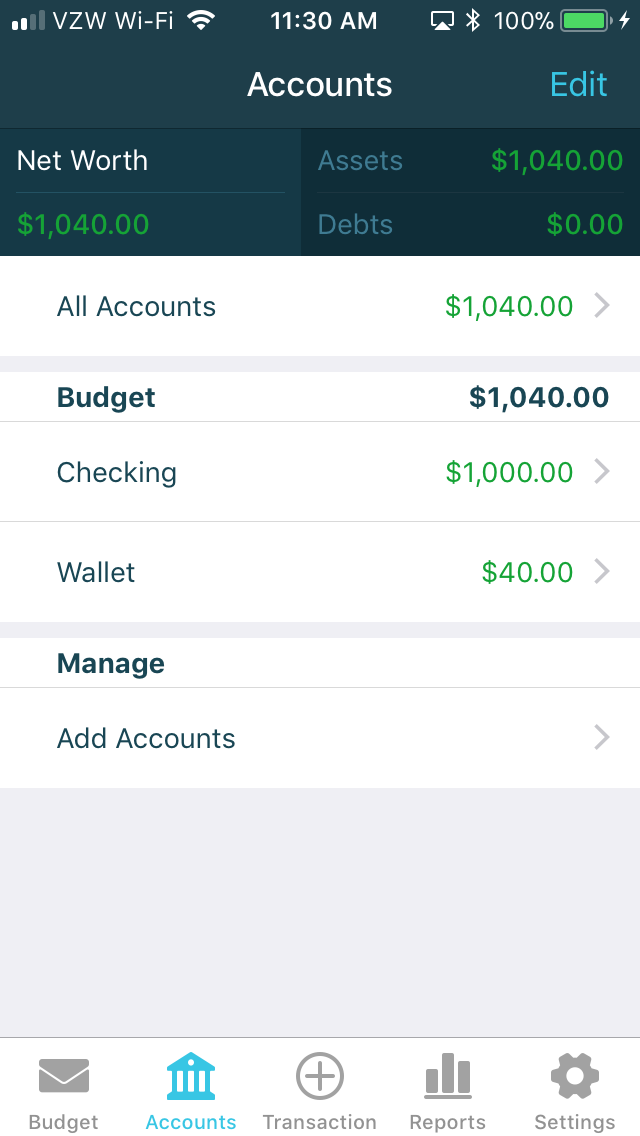

Option 2: The ‘Cash’ Account

Now, if you’re trying to build awareness around your spending habits, use a lot of cash, or simply prefer a detailed record of your expenditures, then Option 1 probably isn’t your best bet. Instead, try a ‘Cash’ account. It works like this:

Step 1

Create a new account in YNAB that will represent the cash in your wallet. We’ve titled ours “Wallet”:

Step 2

Whenever you make a purchase in cash, record it it your cash account. Categorize your cash transactions according to the affected budget category.

So, for example, if you score a sweet, five-dollar end table at a garage sale, you’d record it under your ‘Yard Sales’ category in the ‘Wallet’ account, like this:

Your budget is immediately updated, and you’ve got a record of where that money went. This is useful when you’re trying to optimize your spending habits. For example, if you’re trying to cut back on how much you spend at yard sales, you can look at your budget for the running tally.

Step 3

When you add cash to your wallet in real life, don’t forget to update your cash account in YNAB. For example, if your grandma slips you a crisp 20-dollar bill, you can add that to your cash account as income.

And if you withdraw money from your bank account, record it as a transfer, like this:

Save the transaction, and you’re good to go! Now you can see that cash in the “Wallet” account:

What About Cash Back?

Let’s use our example from above—where we’ve spent 50 dollars at the grocery store and requested 20 dollars cash back. Again, record a split transaction. The difference, this time, is that the cash portion needs to be transferred to the ‘Wallet’ account. It looks like this:

If you’re using this approach, you may find it helpful to pin your frequently used categories to the top of the mobile app.

Which Is Right for You?

If you’re not sure which option of cash management is for you, start with Option 1: the category approach. Time will tell if you need more detail.

… and definitely don’t try to do both options at once. That’s just asking for confusion! Keep things simple, and budget on!