.png)

.png)

.jpg)

Wondering how tracking accounts work in YNAB? Read or watch below to find out!

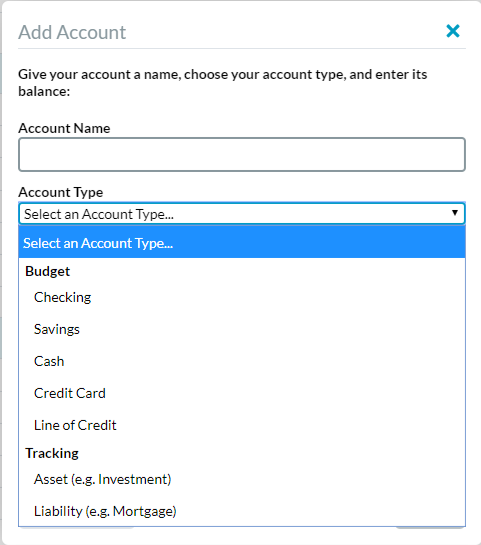

Under the “Add Account” menu in YNAB, you may have noticed the tracking account options: Asset accounts and Liability accounts.

Today, I’m going to walk you through what these account types are for, and talk about why you might do better to just ignore them!

You Don’t Need Tracking Accounts to Budget

We don’t talk about tracking accounts much, because they’re not necessary for budgeting. Take my mortgage payment (please!). But, seriously, think about it—when it comes to your mortgage payment, what really matters? The answer, of course, is that you make the payment. You allocate dollars to your ‘Mortgage’ category, pay it by the due date and you’re done.

You could include a tracking account for your mortgage in the budget, but it doesn’t actually affect your budgeting decisions because:

- Inflows to the tracking account won’t add money to your budget, and

- Outflows from the tracking account don’t come out of the budget.

Your budget doesn’t know anything about the money in your mortgage tracking account. In fact, if you take a look at the tracking account register, you’ll notice that something’s missing:

… do you see it? (It’s what’s not there between “Payee” and “Memo.”)

There’s no category column! And there’s no category column (like you’ll find in your bank account register, for example), because nothing that happens in your tracking account affects your budget.

All that tracking accounts are good for is, well, tracking—specifically, the rise and fall of the account balance. Now, while tracking accounts do not affect your budget, they do reflect in your net worth. So, if you like seeing the true value of your net worth, that is one reason you might like to use tracking accounts.

If you like to keep things simple, don’t worry about tracking accounts and just focus on your budget. If you’re way-deep into personal finance nerdery, then you might enjoy tracking accounts for the insight into your net worth. And, if you’re new to budgeting, skip them! You can always add tracking accounts into your budget later, once you’ve got the hang of things.

Personal Finance Nerd? Right This Way …

So, you want to try out tracking accounts? We’ve got two flavors:

- Asset accounts: Asset accounts include, well, assets! It’s for the good stuff, like investment accounts – 401(k)s, IRAs, or other brokerage accounts – or maybe a hard asset like fancy jewelry, a car, or real estate.

- Liability accounts: The not-so-fun neighbor to asset accounts are liability accounts. These include any debts aside from a credit card or line of credit. The option is there for stuff like mortgages, student loans, car debts (oh my!).

How to Keep Track of Your Tracking Accounts

Before we go any further down this rabbit hole, let me warn you: adding tracking accounts to your budget will add more work for you to do (and, again, they’re completely unnecessary!).

Still here? Oh, you are a personal finance nerd. We’d get along, I’m sure. OK, so to stay on top of your tracking accounts, is to pick a cadence that makes sense to you, and update the balance manually with an adjustment transaction.

I like to update my tracking accounts on a monthly basis. Some people do it less than that. So, for example, if you update your mortgage tracking account on a monthly basis, you’d record an adjustment transaction in the tracking account register to show the difference in the mortgage balance—likely an outflow in the amount of your monthly mortgage payment, like this:

You’ll handle transfers and payments from budget accounts just like any other transfer in YNAB—with one major caveat. Unlike when you transfer between two budget accounts, you will need to enter a category, because the money is leaving your budget. See the bank account register, below:

The savvy among you may be wondering, “What about interest?”

Good question. If your transfer represents a loan payment, some of that is just interest, right? Since most banks don’t separate the interest charge, the best thing to do is transfer the whole payment amount. Then you’ll handle the interest with an adjustment, later on. So, if you accrued 55 dollars in interest on the account, you’d add an outflow to the mortgage register, like this:

Still Unsure About Tracking Accounts?

I offer you, dear reader, the freedom of choice. There’s no one right way to budget, even if there are four very helpful, tried-and-true rules for formulating your perfect plan. Remember, tracking accounts are a trade-off—more insight into your net worth is great, but you’ll have to do extra work to keep your data current.

If seeing your net worth will spur you to change your behavior and achieve your financial goals, even sooner, it’s probably worth the effort! But if all this extra accounting isn’t going to change your mindset or your attitude, don’t bother with it. Above all, if you’re just getting started, start simple, and always keep your focus on the most important decisions—the ones that happen in your budget.